$4 gas: The problem is not Supply.

April 25, 2011

![]() Before Air Force legend Chuck Yeager broke the “sound barrier” in 1947, people believed that it just couldn’t be done. Many (many) died trying, and the conclusion was that “eventually you reach a point where the air just can’t move out of the way fast enough”. The pilot, it was believed, eventually flies into a solid brick wall of air. Of course, that wasn’t true, and today, pilots routinely travel at mach 1x, 2x… even 5x the speed of sound.

Before Air Force legend Chuck Yeager broke the “sound barrier” in 1947, people believed that it just couldn’t be done. Many (many) died trying, and the conclusion was that “eventually you reach a point where the air just can’t move out of the way fast enough”. The pilot, it was believed, eventually flies into a solid brick wall of air. Of course, that wasn’t true, and today, pilots routinely travel at mach 1x, 2x… even 5x the speed of sound.

In 1954, British long distance runner Rodger Bannister did what everyone said was impossible: running the mile in under 4 minutes. To do that, a person must maintain an average running speed of at least 25 (Correction: 15) mph, a feat many came close to achieving, but no one was ever quite able to break “the 4-minute mile” barrier. This led scientists to believe that the human body just wasn’t capable of sustaining such a high rate of speed for the time it takes to run a full mile. But today, now that we know it can be done, athletes routinely break the “4-minute mile”, with the current world record coming in at a scant 3:43.13.

Under President Bush, not only did gasoline break the $2/gallon threshold for the first time in history, but then $3/gal, and eventually $4/gal by July of 2008. Once those “glass ceilings” had been busted, even after sinking back down to under $2/gal by the time President Bush left office, it was going to be MUCH easier to climb back up to those heights the next time around. (I don’t know about you, but whenever I watch and old action movie from the 70’s or early 80’s, I catch myself looking for gas stations to see what the price of gasoline was back then):

Scene from Smokey & The Bandit (1977) – 47cent diesel

On Fox News Sunday (natch) yesterday, host Chris Wallace pointed out that “On the day Barack Obama was sworn in as President, the national average price for a gallon of gasoline was $1.87 a gallon. Today, it is $3.84/gal.”

Yes, but Wallace conveniently omits the fact that just six months earlier, gas prices broke the $4/gallon mark for the first time in history. Don’t try and suggest everything was sunshine & roses up until Barack Obama took office, Chris, because we know better.

During the Summer of 2008, Republicans everywhere were chanting “Drill baby, drill!”, arguing that the solution to gas prices was to open up previously “off-limits” (ie: environmentally sensitive) regions in the United States to increased domestic drilling. Critics pointed out all the flaws with that argument (other than the obvious ecological impacts): It would be years before these new wells would produce a single drop of oil to affect prices, and that there’s just not enough oil in these areas to have any significant long term impact on the world price of oil (let alone the price of gasoline). And now that gasoline is once again flirting with the $4 mark, we are once again hearing… even from President Obama… calls for increased domestic drilling.

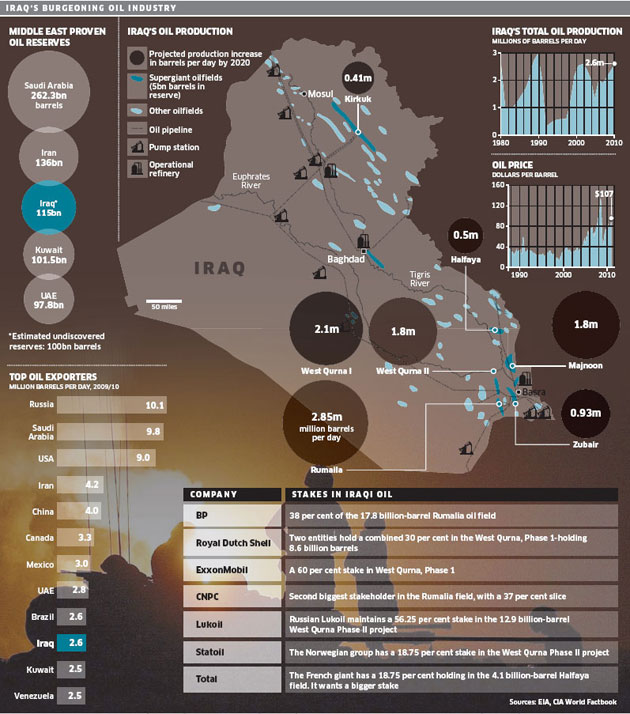

Last week, the following graphic was released showing how all the major oil companies, prior to the invasion of Iraq, were already carving up Iraq’s oil fields amongst themselves, drooling over all that luscious oil:

(Click to Enlarge)

This does not come as news to those of us who’ve seen this particular video from our archive from the January 9, 2004 edition of “60 Minutes”

Looking at the prior chart, one particular stat jumped out at me: that bar graph in the lower left. The third largest exporter of oil in the world is The United States, exporting more than twice as much oil as fourth-place Iran. We constantly dwell on how much oil we import from countries like Iraq and Iran, but the fact is, we export far more oil than we import. It almost seems nuts to import oil when we’re shipping it out at more than twice the rate. But it also highlights one crucial fact: the problem isn’t a scarcity of oil. The price of gasoline isn’t high because there’s not enough oil in the world.

Libya, whose oil Donald Trump thinks we should “just take” in exchange for aiding their rebellion, doesn’t even make the Top 12, producing less than 2% of the world’s oil. By comparison, Alaska produces 8% of the worlds oil (5 million barrels a day)… more than THREE TIMES the amount Libya exports every day (1.5million barrels).

The problem is not supply…

…it’s Wall Street… or to be more specific, oil commodities traders, speculating on the price of oil. In 2008, it was President Bush’s constant saber-rattling over Iran’s evolving nuclear energy program that was stirring up fears of war with Iran, with America (or Israel with America’s help) possibly bombing Iran’s first nuclear reactor before they could finish construction, almost certainly triggering (another) artificial “shortage” by an angry OPEC seeking to teach the U.S. a lesson.

This time around, it’s President Obama’s intervention in Libya that triggered the sudden spike in oil prices caused by Energy Traders on Wall Street, following weeks of violent protests in Egypt… home of the crucial Suez Canal. Once again, unrest in the Middle East has oil speculators in a tizzy (NOT a panic), driving up prices in a deregulated market and putting an already fragile Global Economic Recovery in jeopardy.

President Carter warned the U.S. of the danger of becoming too dependent upon foreign oil from such an unstable region of the world. And yet, Republicans STILL love to hyperbolically pronounce Carter “the worst president in U.S. history” (even worse than James Buchanan, the lead-in to the Civil War?) And of course, I crunched the numbers nearly a year ago, showing that, not only was George W. Bush the worst president since Herbert Hoover, but that Carter produced more than twice as many jobs in four years than Ford and both Bushes did in 15, at a tiny fraction of the cost to the National Debt.

In late June, early July, President Obama has an opportunity to bring Commodities speculators under control when the deciding swing vote on the Commodities Futures Trading Commission (CFTC), a Bush-appointed Conservative Democrat that denies speculation has the power to affect prices, is replaced when his term ends in June.

The problem with $4/gal gas is not Supply. It’s speculators on Wall Street. And once that $4 barrier was broken, any stigma over pushing prices that high again was broken as well. It’s also worth pointing out that the last time gasoline hit $4/gal, the price of oil reached $147/barrel. Today, the price of oil “only” $112/barrel, yet gasoline is already nearing the $4 mark. The answer to reducing oil prices isn’t “Drill baby, drill”, it’s “Regulate (Wall Street) baby, regulate.”

|

Please REGISTER to post comments or be notified by e-mail every time this Blog is updated! Firefox/IE7+ users can use RSS for a browser link that lists the latest posts! | |

|

||

April 25, 2011

·

April 25, 2011

·  Admin Mugsy ·

Admin Mugsy ·  2 Comments - Add

2 Comments - Add

Posted in: Economy, Energy Independence, myth busting, Politics

Posted in: Economy, Energy Independence, myth busting, Politics

2 Responses

I rented a VW TDI last month while visiting Spain and Diesel was comparable to $7.25 a gallon here. However, my rental car, a VW diesel, averaged over 45 miles per gallon and I didn’t feel much shock at the gas pump. This is about a dollar more than the last time I rented a Mercedes A-Series Blu-Tec diesel in 2007 in Frankfurt, which I drove on a 2000 mile trip through France, the Benelux, and Netherlands. For some reason, unlike the USA, gasoline is always a bit higher priced in Europe and was equivalent to $7.50 a gallon last month in Spain. But, during the the three weeks I spent in Spain and Portugal, I never heard anyone bitching about fuel prices. With 20% unemployment, I was most surprised that there was no doom and gloom. Did witness a “red flag” demonstration in Lisbon, a loud, but small crowd and told it was mostly to protest an increase in prices, especially food.

There are no gas hogs on the highway in Europe, everyone driving small but great little cars. Anything larger than a Ford Focus was a head turner. I fell in love with my VW TDI and considering buying one as my next car here in Houston. When I first started driving in Spain in early March, the speed limit was 120 kph (75 mph) but in the interest of the economy, conservation and the environment, the Spanish government lowered the top speed to 110 kph (68 mph). In the meantime, Texas Republicans wish to raise our top limit to 85 mph on some highways here (so there must be plenty of fuel here for our big “dualie” pickup gashogs…yea, more pollution, more highway deaths!).

Everywhere in Spain, I saw highways/bridges being built, or upgraded everywhere meaning JOBS in a nation that sorely needs them. Here we can’t tax the rich in order to keep out people employed! Most of the cost of fuel in Europe is due to taxes which are then spent on infrastructure and mass transit. I didn’t find a pot hole on any of the 700 miles of road I drove on in Spain…great highways everywhere, even secondary roads. Spain is lowering the price of tickets on the state-owned Renfe Railroads, to encourage people to use more mass transit. I mainly rode on trains in and around Barcelona that were clean, fast, and cheap. I followed the new high-speed railbed to Madrid with bullet trains zooming by me at over 200 mph. Everywhere are windmills that now generate 20% of Spain’s power. Don Quixote would have gone out of his mind “tilting” at them!

But for the average American, who has never left his state, even his county, the rest of the world is “Third World” and “evil Socialist Europe” is full of Eurotrash. If they ever had the good fortune to travel elsewhere, it might hit them that they will see very little trash strewn about, the modern cities are surprisingly clean with little visual pollution from billboards to obese people. Although there are pastelerias selling pastries on every block in Spanish cities, people seemingly eating/drinking all of the time in cafes and at sidewalk tables, many city centers are pedestrian-only, traffic-free zones meaning one has to WALK which keeps most everyone slim.

Oil companies cut back exploring, drilling, building new refineries by the end of the Bush administration. But the actions of the oil companies in 2008 may have led to the increase in oil prices again…

“But the project delays [2008] are likely to reduce future energy supplies — and analysts believe they may set the stage for another surge in oil prices once the global economy recovers.”

http://www.nytimes.com/2008/12/16/business/16oil.html

Leave a Reply