Sorry Right Wingers, the Health Care Penalty is NOT a “Tax”. Roberts says so.

July 2, 2012

![]() Everywhere I turned last week, it seemed someone on the Right was calling the “penalty” enforcing the Affordable Care Act a “tax”, and citing Chief Justice Roberts’ written Ruling as their evidence. George Stephanopoulos of ABC’s “ThisWeek” yesterday appeared to spend the entire show obnoxiously trying to make the case this is “a tax”, repeatedly citing the Roberts decision as “proof” (even laughing at one point at the idea anyone might think otherwise). It’s nonsense of course. The ruling makes no such claim. It DOES compare the penalty to a tax, and cites the AUTHORITY to impose a penalty as coming from the same place as the power of the Federal Government to “tax”, but never outright calls it “a tax”. In fact, Roberts goes out of his way to explain how a “penalty” is NOT a tax.

Everywhere I turned last week, it seemed someone on the Right was calling the “penalty” enforcing the Affordable Care Act a “tax”, and citing Chief Justice Roberts’ written Ruling as their evidence. George Stephanopoulos of ABC’s “ThisWeek” yesterday appeared to spend the entire show obnoxiously trying to make the case this is “a tax”, repeatedly citing the Roberts decision as “proof” (even laughing at one point at the idea anyone might think otherwise). It’s nonsense of course. The ruling makes no such claim. It DOES compare the penalty to a tax, and cites the AUTHORITY to impose a penalty as coming from the same place as the power of the Federal Government to “tax”, but never outright calls it “a tax”. In fact, Roberts goes out of his way to explain how a “penalty” is NOT a tax.

“So what?” I hear lots of people respond. “What does it matter if you call it ‘a tax’ or not? If it walks like a duck and quacks like a duck…”. I must have heard that metaphor a half dozen times. What does it matter? Plenty. It’s more than just a matter of semantics. As Senate Minority Leader Mitch McConnell pointed out on “Fox news Sunday” yesterday, the power of Congress to REPEAL “ObamaCare” using Reconciliation depends entirely upon whether or not the penalty is indeed “a tax”:

[flv:http://www.mugsysrapsheet.com/4blog/video/McConnel-Reconciliation_to_repeal_ACA-120630.flv http://www.mugsysrapsheet.com/4blog/video/McConnel-Reconciliation_to_repeal_ACA-120630.jpg 512 288]Senate Minority Leader Mitch McConnell, Fox News Sunday (6/30/12)

If Republicans are able to convince enough Democrats that the “penalty” is in fact “a tax”, then Congress can then legally use “Reconciliation” to repeal the entire law. And that’s what this whole “is a tax”/”is not a tax” debate comes down to: the power to repeal ObamaCare.

While the White House… and President Obama specifically… repeatedly denied accusations that the penalty is indeed a tax, lawyers defending the law before the Supreme Court used every argument available to them that the government does indeed have such enforcement powers, including that the argument that the AUTHORITY to levy “a penalty” is derived from “the same place” the government derives its “power to tax” (from page-1: “this penalty…shall be assessed and collected in the same manner” as tax penalties. §§5000A(c),(g)(1)”). And therein lies the rub.

Reading through most (but not yet all as of this writing) of Justice Roberts’ 150 page decision (pdf), the first 12 pages or so is dedicated to rebuking the White House claim that they have the authority to impose penalties under “the Commerce Clause” (a position Liberal justices, Kagan, Breyer and Sotomayor also rebuked), but then the Chief Justice clearly went to great pains to illustrate why the penalty is LIKE a tax, but in fact is NOT one. A few examples:

“Amicus contends that the Internal Revenue Code treats the penalty as a tax, and that the Anti-Injunction Act therefore bars this suit.” – page 12.

Translation: Roberts is noting that the Amacus pointed out that if this WERE a tax, the court didn’t even have the right to HEAR the case because Congress’ power to tax is unquestionable. The fact they even TOOK the case proves it’s not a tax.

“We have thus applied the Anti-Injunction Act [of 1867] to statutorily described [sic] “taxes” even where that label was inaccurate.” – page 13.

This is important, because he’s pointing out that, when they referred to “The Anti-Injunction Act” (the law restricting the Federal government’s power over state proceedings) to see if it applied in this case, the term “tax” was repeatedly used to describe things that were NOT taxes. Roberts is pointing this out for a reason: Not everything called “a tax” is in fact one. And why else point that out if he’s not suggesting the same goes here?

“In 1922, we decided two challenges to the “Child Labor Tax” on the same day. … [in the first] Congress called the child labor tax a tax … In the second case, however, we held that the same exaction, although labeled a tax, was not in fact authorized by Congress’s taxing power.” – Pages 33/34

What Roberts is pointing out here is that what someone “labels” something is irrelevant. What Congress called “a tax” in that second case, the Court decided was in fact not. “Labels” are irrelevant. It’s the Court’s job to rule based upon the ultimate “goal” of an action. This matters because five pages later, Roberts points this out:

“The joint dissenters argue that we cannot uphold §5000A [the “penalty” provision] as a tax because Congress did not “frame” it as such. … they contend that even if the Constitution permits Congress to do exactly what we interpret this statute to do, the law must be struck down because Congress used the wrong labels.“ – Page 39

THAT is why Roberts pointed out the irrelevance of “labels” five pages earlier. He then goes on to give an example of how the government could penalize you for not buying “energy efficient windows” (ibid). Roberts uses several examples throughout his opinion to reinforce his case.

(jumping ahead past those examples…)

“And the nail in the coffin is that the mandate and penalty are located in Title I of the Act, its operative core, rather than where a tax would be found—in Title IX, containing the Act’s “Revenue Provisions.”

For all these reasons, to say that the Individual Mandate merely imposes a tax is not to interpret the statute but to rewrite it. – PDF page 150.Translation: Roberts is pointing out that if the penalty WERE a tax, the government would have included it in the section under “taxes”. They didn’t, thus supporting the governments good-faith argument that this isn’t… nor was it ever… intended to be a tax. And to claim otherwise you’d have to physically rewrite the bill to make it say that.

As I just illustrated, any claim that the Roberts Ruling declares the penalty “a tax” is… in his words… rewriting the bill. It doesn’t say that. President Obama didn’t lie (Chris Wallace, I’m looking at you) when he denied the penalty was a tax. And Roberts clearly went to great pains to make the distinction… as well as point out that even in those instances where he referred to it as “a tax”, it shouldn’t be taken literally.

On at least three occasions on ABC’s “ThisWeek”, Steph-O and panelist George Will cited use of the phrase “a tax, not a penalty” in Roberts’ decision as their proof the penalty is indeed a tax. And indeed, that phrase does appear on page 35 of the report. But (surprise, surprise), they took the quote completely out of context. Here’s what it ACTUALLY says:

payment may for constitutional purposes be considered a tax, not a penalty.”

It’s that word “considered” that makes all the difference. Roberts is not saying the penalty IS a tax, simply that for matters of juris pudence, it’s enforced the same way. Roberts uses the term “capitation” (fee for services) early on to make the distinction between a “tax” we pay on things we OWN like capital or property, vs “penalties” the IRS may put on certain behavior (like not paying our taxes. We don’t “tax” someone for not paying their taxes. We fine them. And unlike a tax that applies to everyone, the only people that pay a fine are those in violation of the law.)

And it’s a critically important distinction. Because if they can get enough members of Congress to “admit” it’s “a tax”, then Republicans have added incentive to get to the polls this November and vote in a Republican controlled Senate to begin the “Reconciliation” process to repeal “ObamaCare”. It’s all about the election and regaining control of the Senate. So if you weren’t particularly concerned about the Senate before, you damned well better be concerned now. You thought “contempt hearings against the Attorney General” by a Republican House were nonsense, just wait until they seize the Senate too. Not only would they waste the next four years trying to undo every piece of legislation of the last four (a coup by any other name). but remember what happened the last time we had a GOP controlled Congress and Democratic president? Years of multi-million dollar witch hunts (from Whitewater, to Postage-Gate, to eventually impeaching President Clinton for a dalliance that didn’t even start until LONG after the GOP investigations began.) Investigations that lead to the likes of Newt Gingrich in the House and Henry Hyde (correction, “John McCain”. Hyde was also a hypocrite, but not a Senator) in the Senate (both cheating on their wives at the time) impeaching the president for lying about having an affair.

Do we REALLY want to go down that road again?

(POSTSCRIPT: Something I’ve been pondering ever since the verdict that I’d love some feedback on: Several states, such as Vermont, obtained waivers from The ACA [the Affordable Care Act] in order to establish Single-Payer programs in their own state. I’m wondering… while the Federal government agreed as part of The ACA not to establish its own competing Public Option in the National Exchange, what’s to stop Vermont from offering its own program in the Exchange of another state… eg: Texas… to compete with the private insurance companies, effectively creating a backdoor Public Option? The more people paying in, the more stable a state’s “Public Option” would become, so they have a financial incentive to attempt it.)

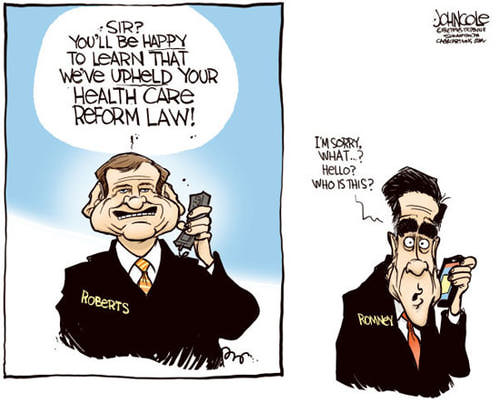

PPS: Uh oh! It looks like ROMNEY also believes the penalty is NOT a “tax”.

PPPS: Hmm, correction. Now Romney “agrees” with the Supreme Court that what President Obama did IS a tax, just not when he did it in Massachusetts (even though he called it one).

|

||

|

Please REGISTER to be notified by e-mail every time this Blog is updated! Firefox/IE7+ users can use RSS for a browser link that lists the latest posts! | |

July 2, 2012

·

July 2, 2012

·  Admin Mugsy ·

Admin Mugsy ·  15 Comments - Add

15 Comments - Add

Posted in: Election, Healthcare, myth busting, Politics, Taxes, Unconstitutional

Posted in: Election, Healthcare, myth busting, Politics, Taxes, Unconstitutional

15 Responses

Not only George on ABC but David “Gotcha” Gregory on Meet the Press argues with Rep. Nancy Pelosi that it is indeed a TAX! http://www.msnbc.msn.com/id/3032608/vp/48031970#48031970 (tax argument at 5 minutes in)In Massachusetts Romneycare only “taxes” 1% of the population because they opt to not buy health insurance.

Yeah, I caught Gregory’s comment as well.It should be noted that, unlike The ACA, RomneyCare actually CALLS their penalty “a tax”. In fact, Romney himself confirmed that fact. I should have included the video, but it would of taken a while to dig it up.

I went back and added video (of McConnell though, not Romney). A link would be helpful if anyone’s got it.

Somewhere George Orwell is laughing hysterically at all the left wing nonsense doublespeak, tap-dance attempts to explain the obvious contradiction here. You and the rest of the Left must be desperate to prevent people from realizing that the Dem congressmen and women (and Obama) lied through their collective teeth to get the ACA passed when they said unequivocally that the “penalty” is not a tax. You also must be feeling pretty insecure about the chances of keeping a senate majority in November and about Obama staying in office or the whole budget reconciliation thing would be a non issue. Ask yourself this “Mugsy”: if (a) the GOP secures a senate majority in November, and (b) attempts to repeal Obamacare using reconciliation, and (c) the Left fights them in court, do you really think the same Supreme Court will rule that now it’s a penalty and not a tax??? Not a chance. If the GOP wins the Senate and the Whitehouse (granted, the odds are long), the ACA will be repealed as will a lot of other legislation. What you call a “coup” is nothing more than the democratic process in action. Oh, and after you get around to finishing Roberts’ opinion, I suggest you read the dissent — especially the parts written by Anthony Kennedy (aka the “moderate” Justice). He thoroughly discredits both the logic and judicial philosophy behind Robert’s decision.

I have to think you never bothered to read the story before posting something so stupid. Standard M.O. for Wingnuts.

President Obama said it’s not a tax. The Supreme Court said it’s not a tax. Ergo, “Obama lied through his teeth”? If anyone is “tap-dancing”, it’s the Right’s desperation to convince us otherwise. Pathetic.

As far as keeping the Majority, my concern isn’t “insecurity”. If you used your head for something other than keeping the rain out of your neck, you’d know there are more Democratic Senators retiring this year than Republicans. That means more races need to be won just to keep the status quo, where as every R pickup is a move toward a shift in control of the Senate.

Regarding your A/B/C questions: If they use Reconciliation to REPEAL the law, it doesn’t go back before the court. The SC doesn’t rule on laws that don’t exist, Frankie Boy.

A runaway Congress that overrules the President and runs the country by proxy… that is indeed a coup. No one ever intended for Congress to run the country.

As for my reading the Dissent, the opinion of the minority doesn’t dictate our laws. If Dissents are that important to you, I suggest you read the Dissenting opinions regarding the recent “Citizens United vs Montana” verdict.

Piss off little boy.

Fact check: Henry Hyde served in the House representing the 6th district of Illinois. He was never in the Senate. Otherwise, good analysis!

Oops, you’re right. I must be thinking of McCain? I’ll make the correction.

Woke up to Fehrnstrom on TeaNN this AM. I thought I was still sleeping when I heard his doublespeak. I see coffee didn’t change what I was hearing…Good job.

Can you clarify something? You point out that ”

We don’t “tax” someone for not paying their taxes. We fine them. And unlike a tax that applies to everyone, the only people that pay a fine are those in violation of the law.)”My confusion is about the word “fine”. The word “fine”, loosely used, can be a synonym for “penalty”. Are you making a distinction between the two words? What is that distinction?Thanks.

In all due honesty, I never considered if there is a distinction between “fine” & “penalty”. I used the words interchangeably. Maybe I shouldn’t have. I’ll have to look into it.

ADDENDUM: Google notes a “penalty” as “punishment” where “fines” are monetary. But since the bill certainly isn’t threatening “punishment” when it speaks of a “penalty” (no criminal punishment), we must assume they used the word “penalty” only in financial terms.

Let me approach it from this perspective: the idea here is that the the “penalty” enforcing the Affordable Care Act is Constitutional because a penalty is not a tax, but it is authorized by the same Constitutional mechanisms that authorize taxes. Is that a good way to rephrase the argument?

For a short “elevator argument” regarding the Penalty:

The IRS is the only part of our government with the power to fine people for being in violation of their financial obligations (other than the criminal court system, but not buying insurance is NOT a “crime”), which is the ONLY reason the IRS is involved in this at all.

Or this: the government can’t order you to buy something, but it can assess a fine if you don’t.If you haven’t guessed, I’m fishing for an argument simple enough to throw down against someone who watches Fox News.

I definitely would not use that argument. It’s not really about purchasing a product so much as “meeting an obligation”.

OK, good point. So to sum up:

The Constitutional argument is that the government does indeed have the “power to fine people for being in violation of their financial obligations”–what the ACA does is make health care insurance a financial obligation. This power just so happens to be grouped under the taxing authority granted in the Constitution (thus, “considered a tax” if in actuality, it’s a penalty). Health care insurance is an obligation because health care is mandatory–everyone gets sick or hurt at some point. And if you don’t have health insurance, basically everyone else has to pay for your health care (because by law hospitals can’t kick you out of their emergency room, which is a good thing) usually through higher costs for care. I think I’ve got it now. I should tell my conservative friends and family, the whole point of the mandate is so that YOU don’t have to pay for someone else who didn’t have the sense to buy health care insurance, and they’d get that (it’s not quite that simple, but still…)

Leave a Reply